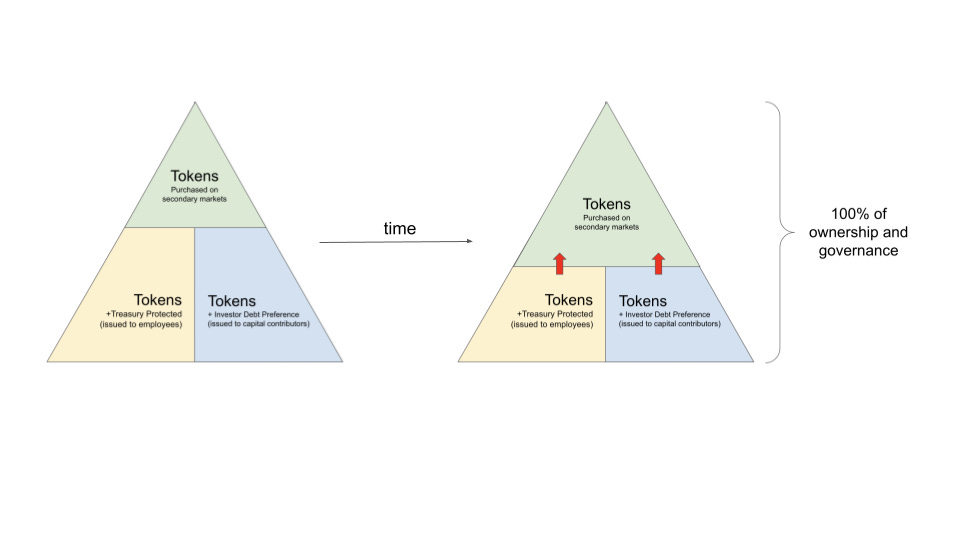

In the treasury-centric model of on-chain organizations, there is only one type of token. The token simultaneously represents governance (voting power) and ownership (in the case of profit-seeking entities). The token of an organization should be thought of like a share of a company, which allows for voting and ownership. Any token purchased on secondary markets has all of these rights, equal to all other tokens. There are no tiers to the tokens that trade on secondary markets– they are all fungible.

While all of the tokens are the same type, the original recipient may be given some additional incentives to align the long-term interests of the operators and investors of the organization. These are Treasury Protected Tokens and Investor Debt Tokens.

Employees/contributors receive Treasury Protected Tokens (TPTs), which the treasury promises to repurchase at a guaranteed minimum price floor. This provides employees 100% equity-based compensation, while guaranteeing a minimum level of compensation in USD-terms. Once this token is traded (i.e. an employee sells it on secondary markets), it no longer has any redemption rights, it is just a standard token. Purpose: provide optimal compensation to recruit the best talent in the industry. Benefit: Pay employees with 100% token (equity) compensation without downside risk, employee exits strengthen the treasury.

Investors receive Investor Debt Tokens (IDTs), which are provided in exchange of capital contributions, generally in the form of USDC. The original recipients of IDTs are given liquidation preference in the event the organization votes to liquidate. That means they’re entitled to the refund of their original contributed capital before profits are distributed among token holders on a pro-rata basis. If an IDT holder sells their tokens on secondary markets. Purpose: provide incentive for original investors to hold the token while providing a hyper-simple rage-quit mechanism. Benefit: No lockup-expiry selling pressure, investors exits strengthen the treasury

When we summarize the characteristics of the tokens, we see that the differences are quite small. As noted above, the tokens issued to employees have the added benefit of “treasury protection” and the tokens issued to investors have the benefit of liquidation preference:

It is important to note that all tokens sold on secondary markets are identical. If an employee sells their token, they are just selling a regular token. The recipient does not receive rights to redemption. Likewise, if an investor sells their token, the liquidation rights do not transfer.

In summary, it is worth re-emphasizing that all tokens are identical. Some people have additional rights upon issuance. These added benefits are non-transferable. All tokens that trade on secondary markets are identical. There is only one type of token.